The mechanics of a Credit card transaction

It's more than just a swipe

At the end of 2017, the average American held 3.1 credit cards with an average balance of $6,354—plus 2.5 retail credit cards with an additional balance of $1,841.

- Experian's State of Credit report

Credit cards have rightly been called the cornerstone of American capitalism. While I mostly used debit cards in India, I never looked back after I started with credit cards in the US. Something about the cashback and the premium benefits is just irresistible. Whether the dopamine hit from the cashback was worth the monetary value loss incurred from incremental spending is a question for another day. I was always fascinated by why it took so long (2-3 days) for a transaction to appear on the final statement. I decided to go down the rabbit hole of this seemingly simple interaction.

History

While some versions of credit cards have existed for a long time, the modern one started out as the Diner’s club card in 1950. A customer named Mc Namarra had forgotten his wallet while attending a business dinner at New York’s Major’s Cabin Grill (Clearly NY was the land of Fintech from then). Side note 2: His wife bailed him out. A few months later, Namarra and his partner proposed a small cardboard card that transformed into the Diner’s Club Card. It had almost 42k cardholders by 1951. Several other companies followed soon such as American Express in 1958.

With time, there has been an explosion in credit card usage and a ton of innovation has happened in the space, though the essence has remained the same.

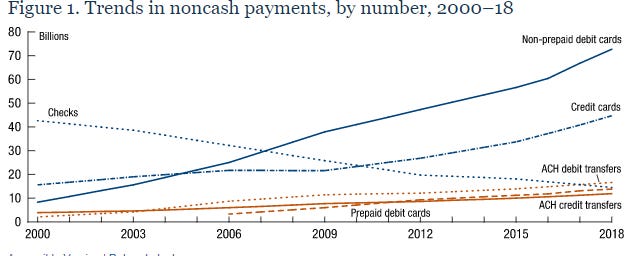

The above image is from the Federal Reserve in 2019 and shows the rise in credit card transactions. Though the latest data is not yet available, it will be interesting to see how the pandemic has influenced the usage of credit cards/ online payments.

The gory details

Let’s now get into the inner workings of the transaction. To begin with, there are four major components of a credit card transaction

Issuer - The bank which issues the credit card to the customer such as Bank of America, Chase

Merchant: The business or store the customer purchases from such as Macy’s or Trader Joes

Acquirer - Roughly, it is the bank associated with the merchant.

Credit card network- Networks such as Visa, Master card which facilitate the transaction

There are a few more parties in the transaction but we will go through them as we go through the transaction. Like you can imagine, the overall goal is to transfer the money from the customer to the merchant. But, let’s complicate it

This shows the flow of the credit card transaction as a customer purchases something at the store using a credit card. Note, this does not have the settlement flow

There are three major stages in a credit card transaction

Authorization

When the customer swipes the credit card at the Point of Sale(POS) terminal, the card details are sent to the acquiring bank(or processor)

The acquiring bank in turn forwards the details to the credit card network(brands)

The credit card network forwards the request to the issuing bank after ensuring the transaction is kosher

Authentication

The issuing bank receives the request from the credit card network

It performs some checks (based on the account balance etc) on the customer’s account and verifies/denies the transaction. The request is sent back to the merchant via the same route.

Once the merchant receives the authorization, the issuing bank places a hold on the cardholder’s account. This shows up in the customer’s credit card account as ‘Pending’

Clearing and Settlement

The merchant sends the list of approved transactions to the acquirer at the end of the day

The acquiring processor then routes the aggregated transaction list to the credit card network for settlement

The credit card network in turn forwards it to the appropriate issuing bank

Within 1-2 days, the issuing bank transfers the funds

The credit card network then pays the acquiring bank which then credits the merchant’s account

The issuing bank also then posts the transaction as final on the customer's account.

A few things to add to the mix

A merchant for the most part has to support all the different credit card networks. Some merchants restrict Discover or Amex but it is rare

Networks such as Amex are unique in the sense that it is both an issuer and an acquirer

The issuing bank is able to offer cashback to the customer to gain the loyalty of the customer and is also liable for the purchases made by the customer

The overall cost of the transaction to the merchant is around 3% and we are going to discuss this later

A lot of work for credit card companies goes into fraud detection and has gotten a lot better over time. If you ever had a transaction denied on vacation, it is most probably the credit card company being suspicious of your suddenly new location (unless you booked the flight tickets using the card, of course)

The issuer consists of the issuing bank and the issuing processor (think Fiserv, Fidelity Information Services). The payment processor on the other hand works on behalf of the merchant banks to process transactions, underwrite merchants, and pay them as well(such as the First world).

An additional part of the ecosystem is the Payment Service Providers(PSP). Payment Facilitators(such as Stripe, Square) are a specific type of PSP. It helps in embedding payments into vertical software. Vertical software essentially boils down to being able to use a single software for the entire flow in a specific industry. This is made possible by companies such as Stripe which serves as a full-stack payment processor not limited to credit/debit card transactions.

“Payment facilitators exist in the middle of a sophisticated stack of networks and organizations that interact to ensure data and funds are safely and securely transmitted from cardholder to the end merchant. Payment facilitators bridge the gap between sub-merchants and acquiring banks and processors while managing risk, ensuring compliance, and simplifying settlements.”

I have skipped over some of the hardware aspects of the working of a credit card. Interested readers can check this out.

The math

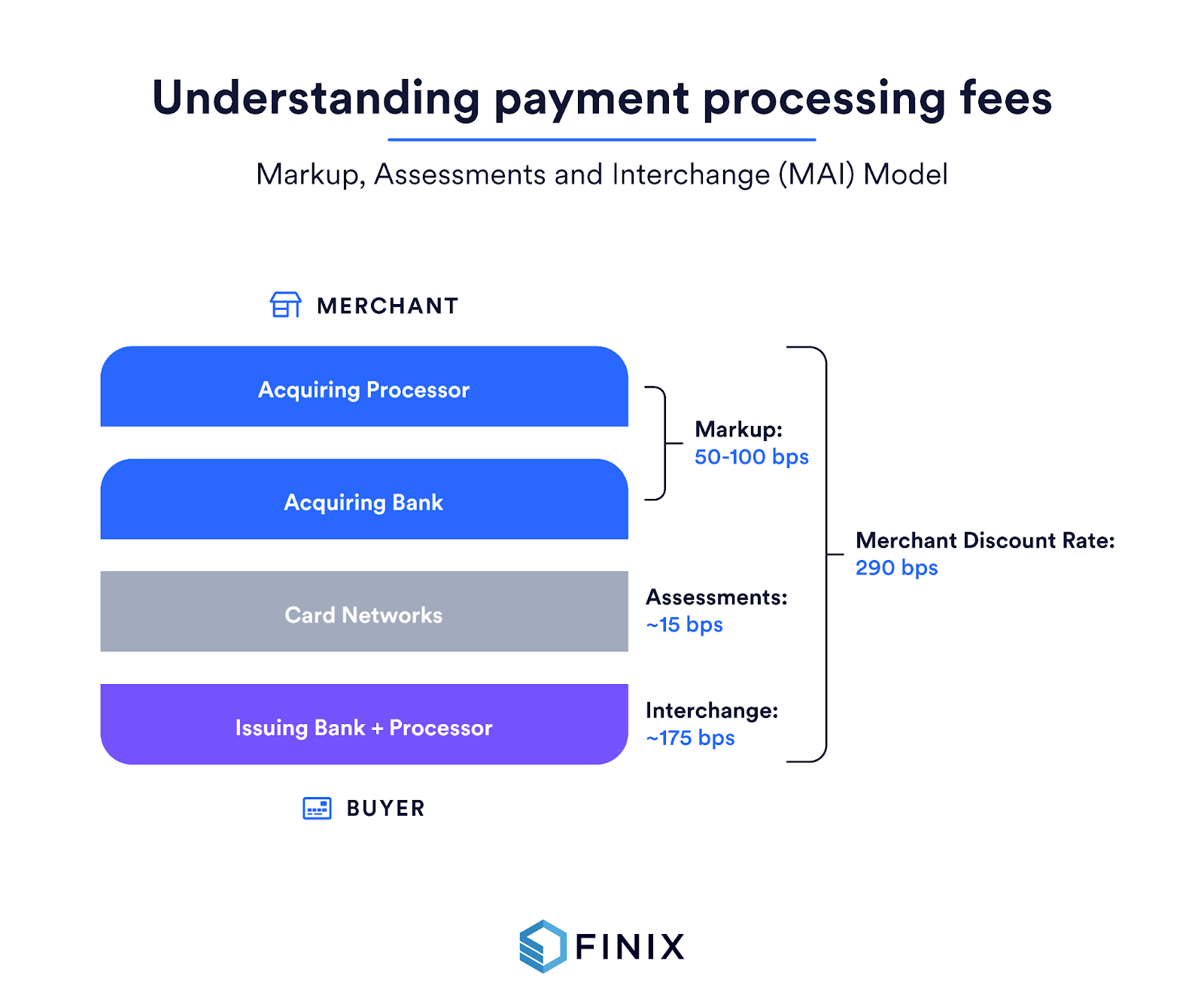

Link: https://blog.finixpayments.com/understanding-payment-processing-fees

The above illustration from Finix Payments does a fantastic job of explaining the economics of a transaction. This model from Finix Payments is called the MAI (Merchants Assessments Interchange) model. A bps refers to 1/100 of a percentage of the gross value of the transaction. As a caveat, the numbers are not exact but a rough estimate.

Markup Fees

The markup fees( aka processor fees) are split across the acquiring bank and acquiring processor. It can either be a fixed percentage or a fixed cost or a combination of both. This accounts for about 20-30% of the merchant discount. Markup fees are negotiable and vary by the company.

Assessment Fees

Also known as due and assessments, they are fixed by the credit card networks twice every year. An example for Visa is here. These fees are non-negotiable. The credit card fees are almost like the proverbial Warren Buffet’s bridge toll.

Assessments typically consist of a percentage fee, a flat fee, and a card network fee (e.g., a cross-border transaction fee) and are often paid on a per-transaction basis for the ability to process transactions on a network’s rails

Interchange Fees

Also known as bank fees, Interchange fees are paid by the merchant bank to the issuing bank. It is shared with the issuing processor and card program manager. Just like the interchange fees, these are non-negotiable and set by the banks twice a year. These fees help the issuing bank offer cashback to the customers (roughly). These fees usually consist of a per-transaction take rate and a fixed flat fee. Various factors determine the interchange fees including the type of merchant, the card network, transaction type.

How is this different from a debit card transaction? Why is there no cashback on a debit card transaction?

The overall flow in both of are them are similar

There are some key differences w.r.t a debit card transaction

The bank is pre-authorized to access the funds of the customer. So all the transactions are final and cannot be disputed. This can be dangerous in cases of fraudulent transactions

The chance of default is very minimal as the funds are actually taken out from the account.

The merchant discount rates for debit and credit card transactions are slightly different.

Finally, there were cashbacks on debit card transactions prior to the Durbin Amendment in the Dodd-Frank Act in 2010. The amendment capped the interchange fees on debit cards and most banks discontinued their cashback offers right after.

Upcoming Trends

There are a few trends in the evolution of credit cards

Contactless payments have now gone mainstream and the pandemic has spiked the usage further.

The Buy Now Pay Later(BNPL) schemes such as Affirm has grown alongside credit cards

Credit card issuing companies such as Marqeta will see a boom as more and more companies chose to issue their customized credit cards (virtual as well)

There is more B2B adoption of credit cards with the rise of expense management companies such as Ramp, Brex. A lot more bundling of credit cards with other products will be seen in the foreseeable future

Will facilities like Apple pay and Samsung pay start eating into the major credit card networks?

What else would you add?

Sources:

https://www.finixpayments.com/blog/understanding-the-payments-stack/

https://wallethub.com/edu/cc/credit-card-transaction/25511

https://blog.finixpayments.com/understanding-payment-processing-fees

https://www.nerdwallet.com/article/credit-cards/where-does-money-for-credit-card-rewards-come-from